How do we Model Markets in Unprecedented Times?

What Systems Neuroscience Can Teach Us About Modelling Financial Markets

It’s no longer enough to look at a headline and use your judgment to make a trade. Before your thought passes through the full process of comprehension, Jane Street’s algo traders have shifted the markets 6 times. That leaves us asking the question, how could I have made that decision faster? This is why concepts inspired by neuroscience, from neural networks to mechanistic models of decision systems, have been adapted into and optimised to fit real-world scenarios like navigation, content creation and trading.

We can approach this in one of two ways:

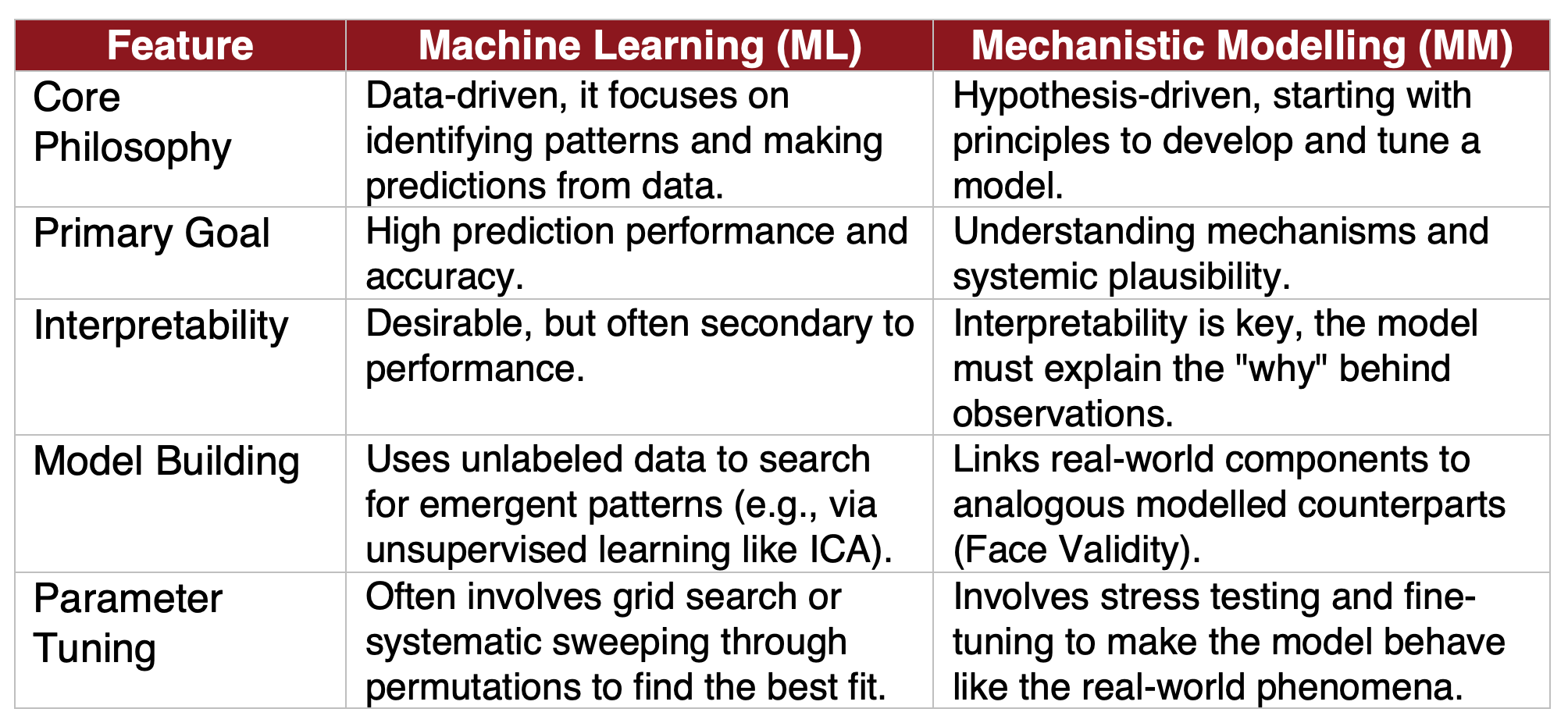

Machine Learning

Mechanistic Modelling

This depends on our goal: do we want a plausible model that works slower or a largely accurate yet sometimes inexplicably wrong model that works faster?

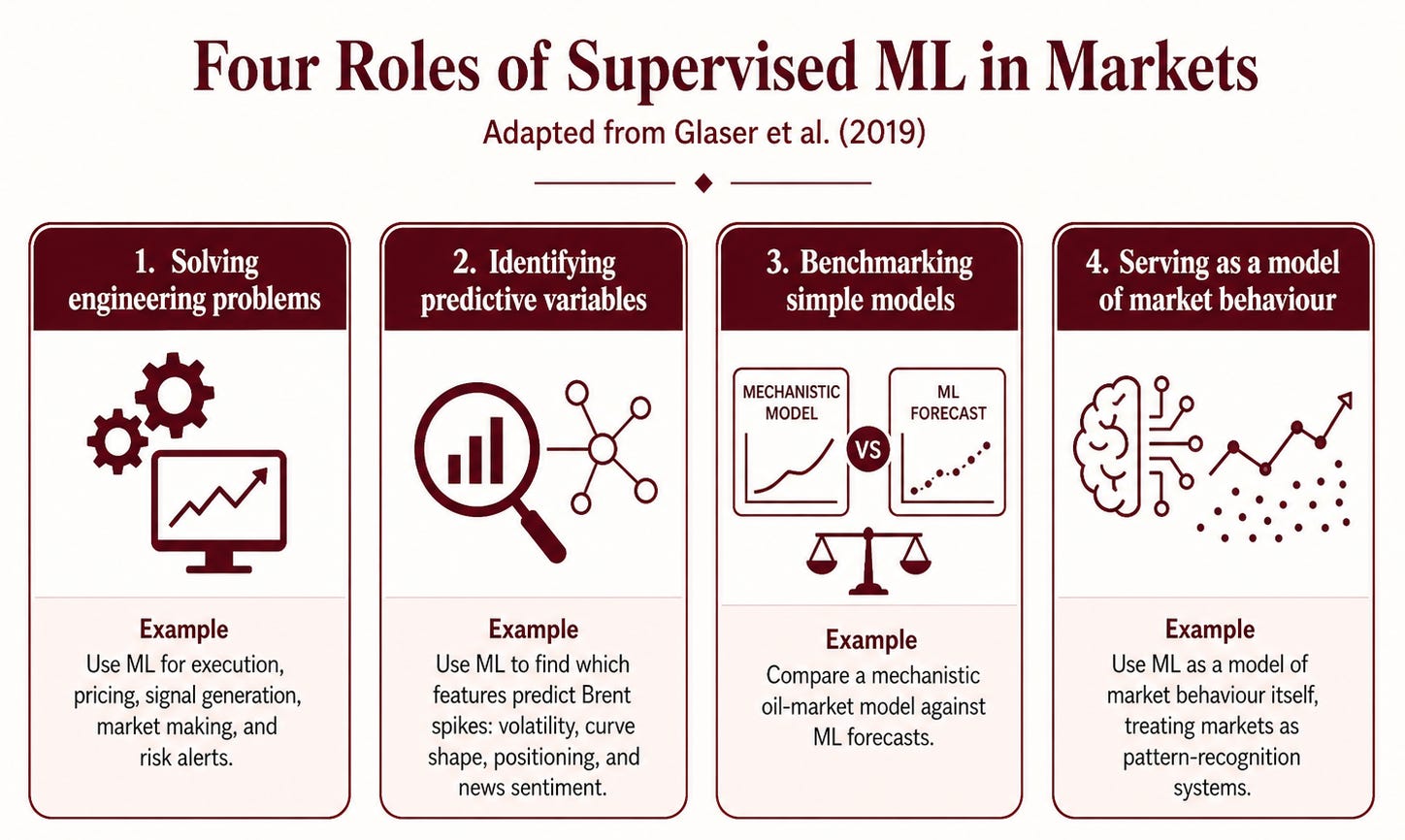

How can we use ML in Markets?

Glaser et al. 2019 defined how we can use Supervised Machine learning in 4 different ways in systems neuroscience. These translate to markets.

The first three roles do not require the model to be a true explanation of the brain. They only require it to be useful. We cannot treat predictive success as understanding here.

Understanding in a Real World Context

Let’s put this into context. It’s Feb 28th 2026, the Iran-US war has just started, and Brent crude futures jumped nearly 7%, briefly hitting $126 per barrel.

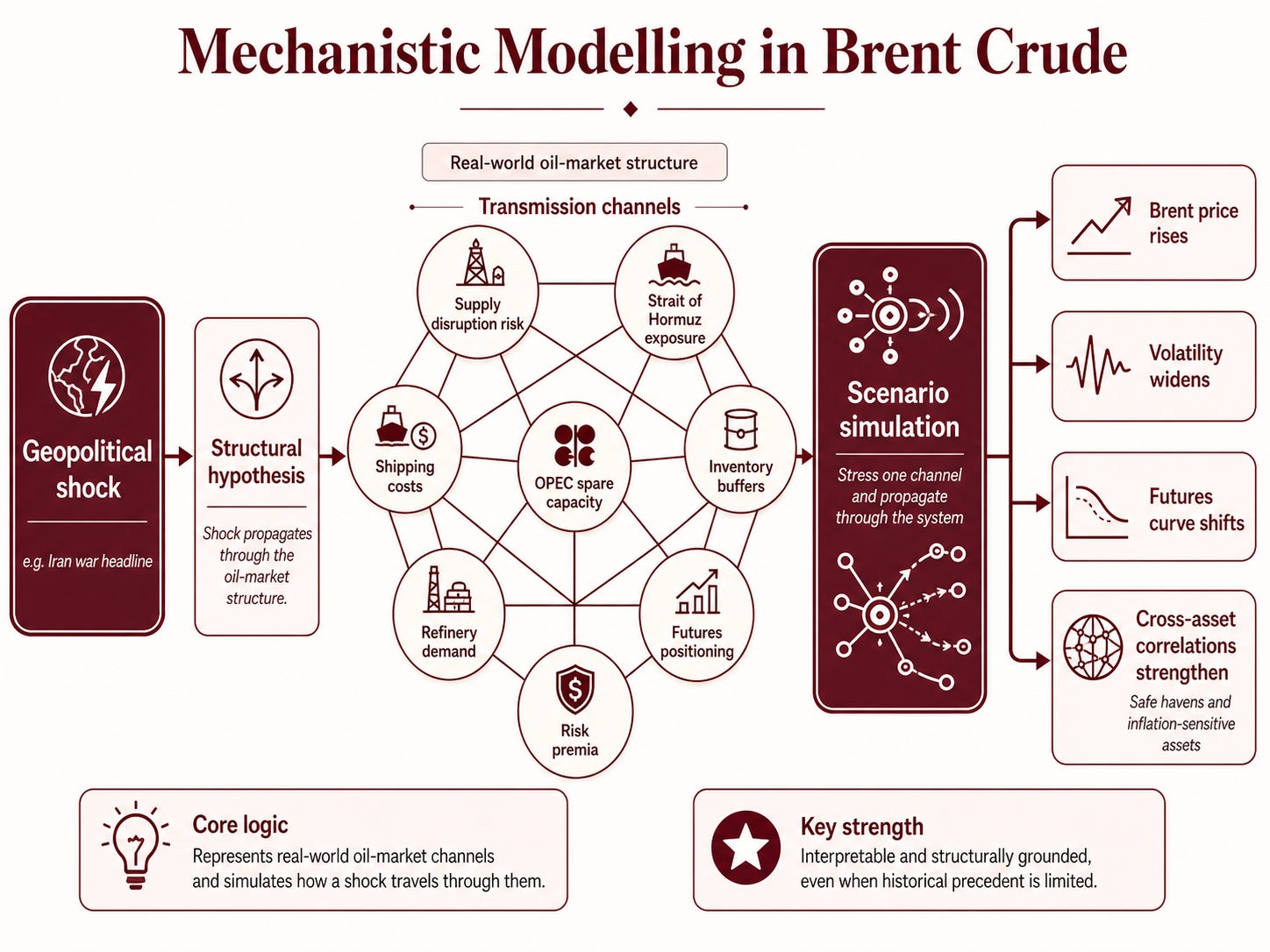

Mechanistic approach

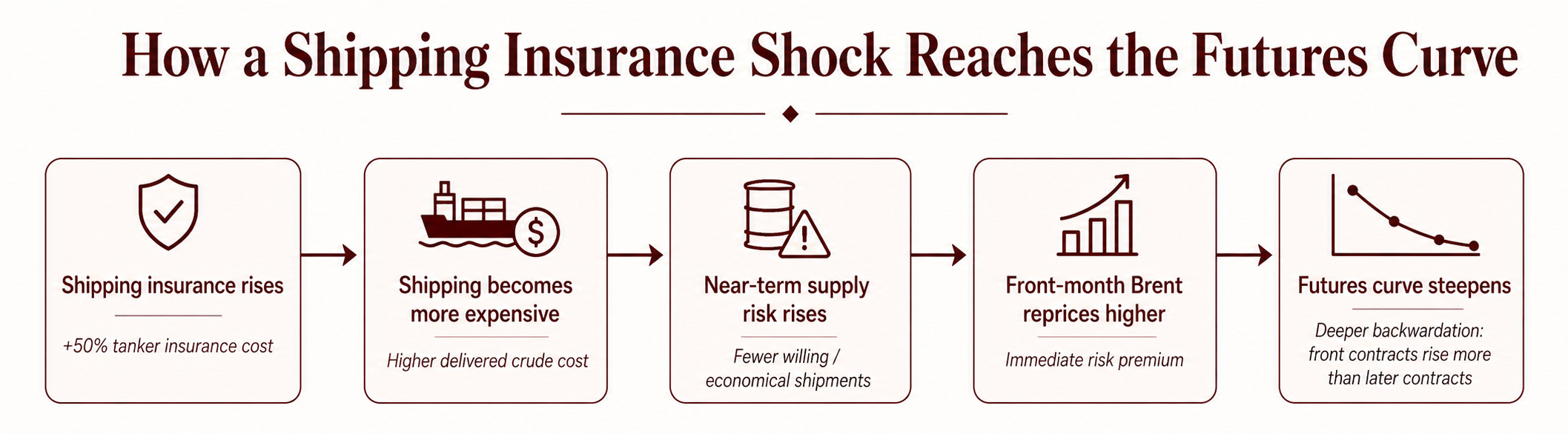

A mechanistic model would begin with a hypothesis about how the Iran war headline affects Brent crude through the structure of the oil market. This would be human-generated. The model would map the real-world transmission channels and simulate how stress to one part of the system changes the behaviour of the wider market. For example, we want to see what shipping insurance increases do to the futures curve.

By seeing a model’s reaction in these scenarios, we are better able to understand the reasons behind shifts in the market.

In neuroscience, even our best computational models rarely get close to reproducing full cognition. Instead, they capture specific circuits or tasks under tightly controlled assumptions and are constantly stress‑tested against new data. In markets, a mechanistic model plays a similar role. It would not be a full digital replication of the global oil system causally, but a deliberately simplified dynamical system that encodes hypothesised causal channels and is updated when it fails. This can be extremely valuable for scenario analysis and for understanding where historical relationships might break.

In the bigger picture, it would look like the image below.

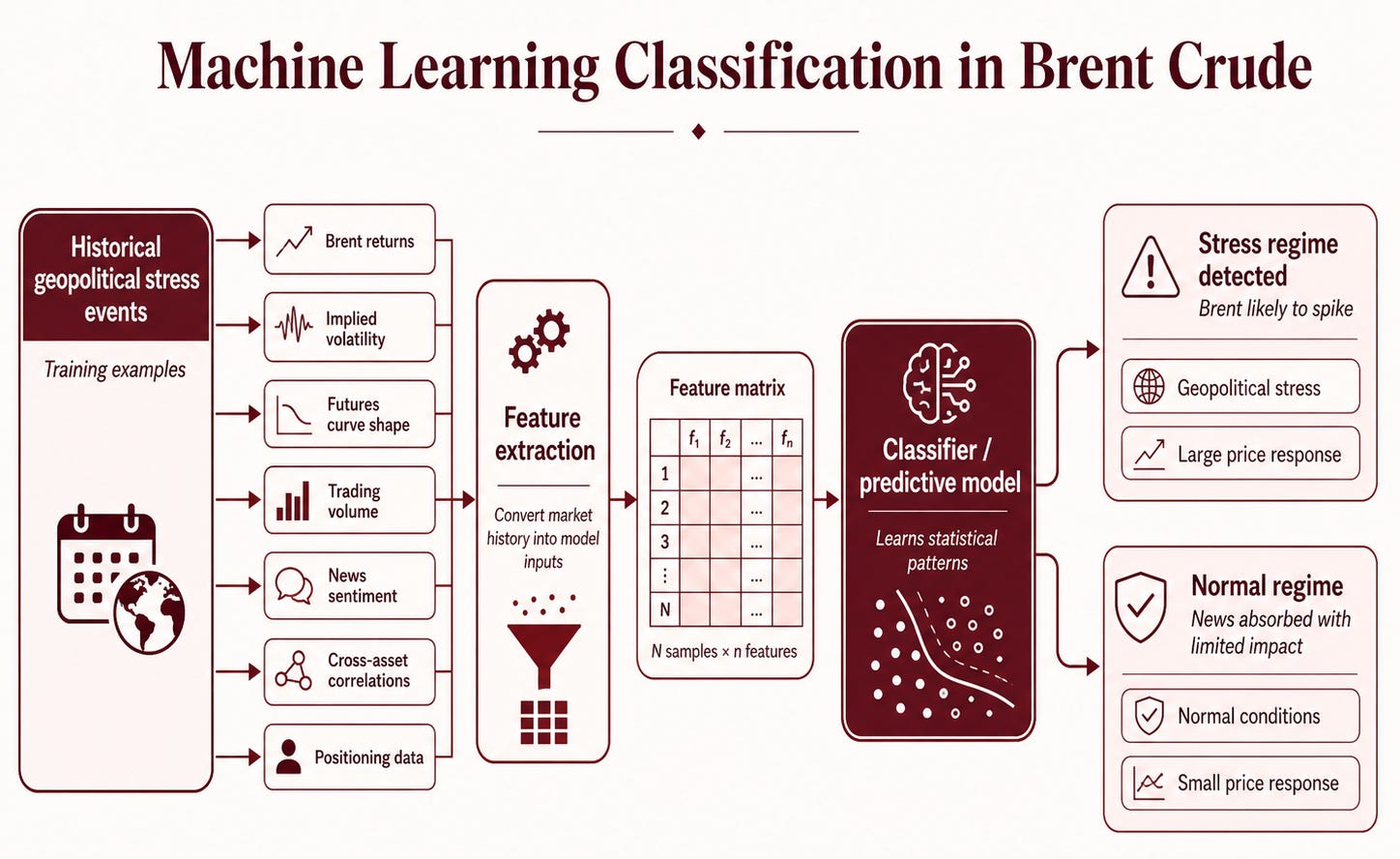

Machine learning approach

A machine learning approach would treat an Iran-related oil shock primarily as a classification or prediction problem. The model would be trained on historical market features surrounding previous geopolitical stress events. The aim would be to identify patterns that distinguish normal market conditions from geopolitical stress regimes, and to learn a decision boundary between periods where Brent crude is likely to spike and periods where the market absorbs the news with limited price impact.

However, these models become vulnerable during black swan events, where the current market does not closely resemble the historical data on which the model was trained. JPMorgan said hedge funds were having their worst drawdown when the war was announced since the prior tariff shock, and Reuters reported that systematic quants like CTAs were hit especially hard. The Wall Street Journal reported that Millennium Management and Point72 each lost about $1.5 billion in one week. In these moments, models may need to be paused or overridden because they are calibrated to historical relationships that break down under extreme uncertainty.

These models are trained on past data; the last time the Strait of Hormuz was affected like this was during the 1980s Tanker War. It was already a critical oil chokepoint, but the market structure was very different. Flows through the strait fell sharply as tankers were attacked, yet the disruption directly affected only a small share of ships, and real oil prices drifted lower regardless through much of the decade. In other words, even a direct military threat to shipping did not translate into a simple, one-directional oil-price shock.

Today, the same type of disruption would travel through a much larger and more financialised system. Around 20 million barrels of oil per day now pass through Hormuz, alongside significant liquified natural gas flows, while Brent has become a global pricing benchmark for a large share of seaborne crude. A Hormuz shock would therefore not only affect Gulf exporters such as Saudi Arabia, Iraq, Kuwait, Iran and the UAE; it would also reprice Brent-linked barrels, shift the global futures curve, and feed into inflation, rates, FX, and risk sentiment.

This creates a fundamental problem for machine learning models: there may be no clean historical analogue. The model can detect statistical similarities between past and present stress events, but it cannot fully understand whether today’s market structure is different in a way that makes the outcome more severe. In a world where geopolitical shocks, inflation concerns, energy security risks, and cross-asset volatility are occurring simultaneously, the model may be forced to make predictions from incomplete precedent.

While an ML model may be useful for detecting whether Brent crude is entering a stress regime, its weakness is that it may not explain why the regime is forming or whether the present shock is structurally different from the past.

Concluding Remarks

However, we can argue that most of the time, we don’t need to know how something works; we just need to know that P&L incrementally compounds over time.

This is the key difference between neuroscience and markets. In neuroscience, interpretability is ethically necessary when someone’s life and livelihood are on the line from the impact of a disease. Money can be made back, but health cannot.

In markets, the cost of not understanding the mechanism is not nearly as severe. It appears as hidden leverage, crowded positioning, false confidence, and models that fail precisely when the market stops looking like their training data. That is why the strongest trading system is not purely machine learning or purely mechanistic modelling.

ML works better when the market behaves like history. Mechanistic modelling works better when the structure changes. The real edge is using both ML for speed and mechanistic modelling for guardrails.

Thank you for reading!

References

Bloomberg News. (2026, March 10). Balyasny, Millennium, Point72 hit by Iran conflict in wild week. Bloomberg.

CNBC. (2026, March 18). Hedge funds suffer worst losses since “liberation day” on Iran war turmoil. CNBC.

Reuters. (2026, March 25). Hedge funds get B-minus in Iran market stress test. Reuters.

Reuters. (2026, April 1). Hedge funds hammered by market turbulence triggered by Iran conflict. Reuters.

J.P. Morgan Chase & Co. (2026, March 12). JPMorgan says hedge funds hit by worst drawdown since April. Business Times.

The Wall Street Journal. (2026, March 10). Iran conflict triggers losses for Citadel, Millennium and Point72. The Wall Street Journal.

An interesting background for this topic is The (Mis)Behaviour of Markets: A Fractal View of Risk, Ruin and Reward" by Benoit B. Mandelbrot. TLDR - there are patterns, but they are not truly predictive of market behaviour, it just looks like it.

Read it a few times. Then ran independent research — not to disagree, but to find where intuition ends and fact begins.

The facts came out stronger.

2025-2026 produced a convergence that's hard to ignore: five independent fields — neuroscience, financial ML, Chinese systemic risk models, network physics, LLM evaluation — independently arrived at the same architecture. The regime detector sits before the model, not inside it. PNAS October 2025 via Kuramoto showed that proximity to a critical transition predicts collapse trajectory — something no return-based model can structurally see.

Millennium and Point72 each lost $1.5 billion not because the models were bad. They fell along a trajectory physics already knew.

What's striking is that neuroscience showed the same thing from the inside: the locus coeruleus isn't part of the predictor — it's a separate system above it that decides when the brain's model is no longer valid and triggers a rewrite.

I'm building exactly this detector — through cross-asset synchronization, not price prediction. A system that knows when to stop matters more than one that always answers.

Your article frames this precisely: the problem isn't technical — it's epistemological. The model doesn't know what it doesn't know.

One question after reading: do you see a difference between how American and Chinese approaches behave at the moment of transition? The data suggests there is one — and it's architectural.